For most of 2024 and into early 2026, Dubai’s millwork and fitout market was already undersupplied and Western contractors were racing to get in. Then came a period of regional macro uncertainty in early 2026. Sentiment shifted quickly and a market that had been sprinting suddenly paused. For millwork contractors in the USA, Canada, and the UK, that pause may represent a wider entry window than it first appears.

There is a particular kind of clarity that comes when a fast-moving market catches its breath. You can finally see who was building for the long run and who was just riding the wave. Right now, Dubai is in that phase of recalibration. What happens in the UAE over the next 18 to 24 months will likely matter to your business more than you might expect.

And here is the striking part: even through this period of uncertainty, the numbers keep coming in strong. Q1 2026 data released by the Dubai Land Department shows total real estate transactions reaching Dh252 billion, a 31 percent year on year increase. The market is consolidating at a higher base.

Table of Contents:

- A Market That Just Broke Its Own Records

- The Fitout Sector: A USD 10 Billion Market With Room to Grow

- A Pause, Not a Retreat

- A View from the Ground

- The Contrarian Case: Why This Phase Rewards Early Movers

- Weighing the Decision: A Practical Overview

- The Millwork Advantage: What Western Firms Bring

- The Question Worth Sitting With

- Sources and Further Reading

A Market That Just Broke Its Own Records

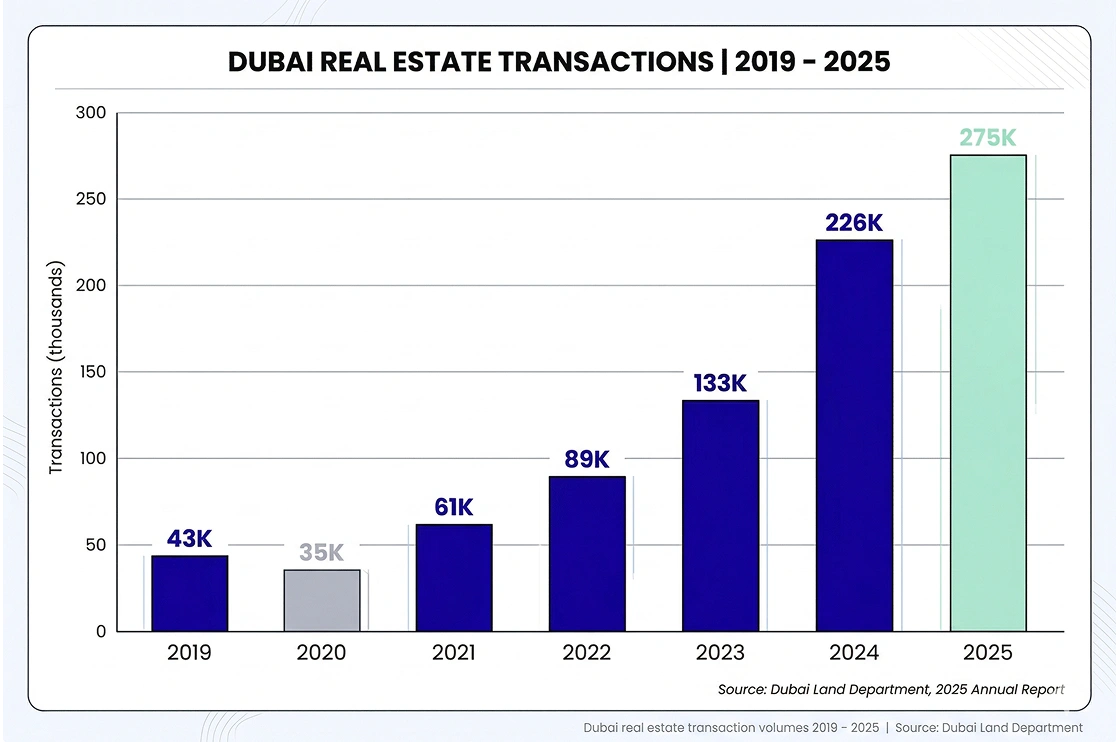

Before the regional macro developments of early 2026, Dubai and the broader UAE were experiencing extraordinary momentum. Dubai Land Department data reflects real estate transactions climbing from 43,000 in 2019 to 275,000 in 2025 [1]. That is not incremental growth. It is a market rewriting its own benchmarks.

Industry forums, seminars, and business conversations across the USA, Canada, and the UK were consistently pointing to fitouts and facility management as the top sectors to establish in Dubai, citing a visible shortage of high-quality fitout execution capacity in the market. Millwork companies from these markets were actively evaluating joint venture structures and local entry strategies.

Then came Q1 2026 [2]. Even with a period of slower approvals in March, the quarter still posted record-level results:

Market snapshot: key indicators through Q1 2026

| Indicator | Data Point | Source |

|---|---|---|

| RE transactions 2019 to 2025 | 43,000 growing to 275,000 (up 540%) | Dubai Land Department and DMO1 |

| Q1 2026 total transactions | Dh252 billion (up 31% year on year) | Dubai Land Department, Apr 20262 |

| January 2026 sales | AED 72.4B, the highest single month ever recorded | fam Properties and DLD4 |

| New investors Q1 2026 | 29,312 new investors, up 14% year on year | Dubai Land Department3 |

| Residential price growth | Up 20% in 2024 and up 12.5% year on year in Q1 2026 | Deloitte 2025 and fam Properties |

| Office rent growth | Up 17% year on year in 2024 | Deloitte 20253 |

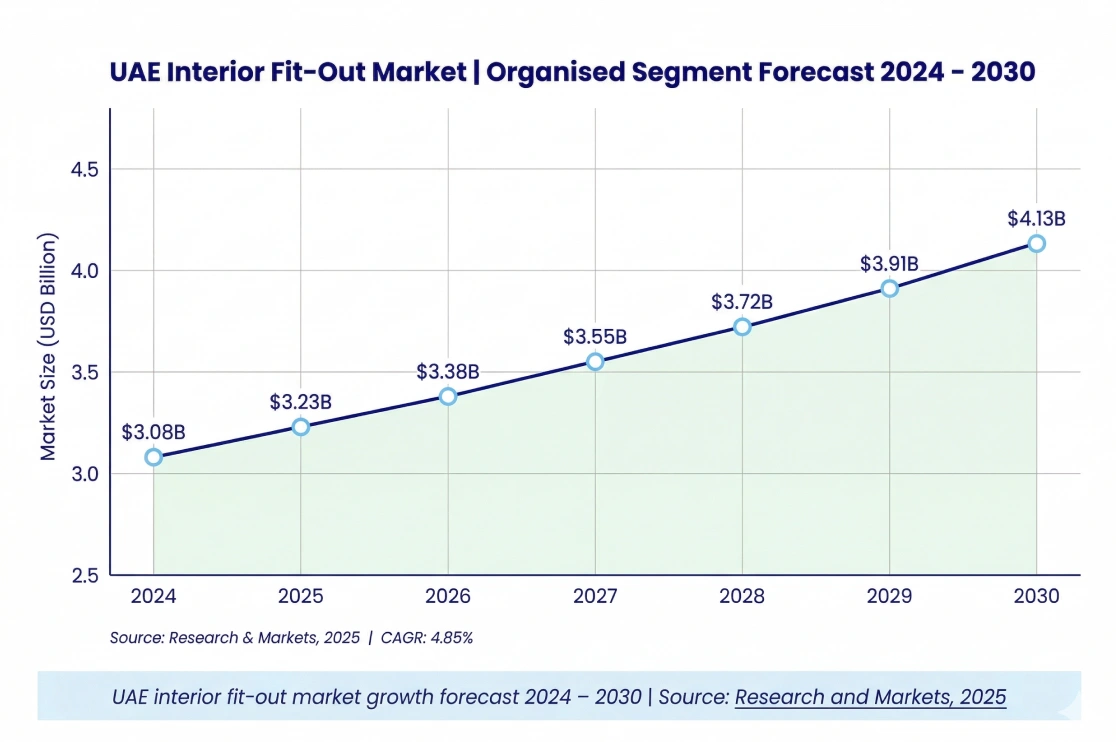

| UAE fit-out market size | USD 10 billion as of 2024 | Research and Markets10 |

| Organised fit-out growth | USD 3.08B growing to USD 4.13B by 2030 at 4.85% CAGR | Research and Markets10 |

| Dubai interior design share | Over 52% of total UAE market | Mordor Intelligence, 202512 |

| Hotel construction pipeline | Over USD 100B underway including Aman, Janu, Rosewood | Mordor Intelligence12 |

| UAE GDP growth forecast 2026 | 5.0%, the fastest rate in the GCC | IMF via Edwards and Towers17 |

Sources: Dubai Land Department, Deloitte 2025, fam Properties, Cushman and Wakefield Core, Research and Markets, Mordor Intelligence, IMF

Dubai Real Estate Transaction Volumes 2019 to 2026 | Source: Dubai Land Department and DMO

January 2026 alone recorded AED 72.4 billion in sales, the highest single month in the history of Dubai real estate. Off-plan properties accounted for 70 percent of total Q1 transaction volume, reflecting deep developer pipelines and sustained buyer confidence in the city’s long-term trajectory.

These are not vanity statistics. They represent real property being bought, designed, and fitted out, creating a downstream workload in millwork and interiors that the local market cannot fully absorb on its own. For more on what this means for contractors, let’s dive in.

The Fitout Sector: A USD 10 Billion Market With Room to Grow

Research and Markets data[12] published in early 2026 values the total UAE interior fit-out market at USD 10 billion as of 2024. The organised segment sat at USD 3.08 billion, growing at a 4.85 percent CAGR toward USD 4.13 billion by 2030. Dubai holds over 52 percent of UAE interior design market share and is expanding faster than any other submarket in the region.

Beyond the headline numbers, the hospitality pipeline alone is substantial. Mordor Intelligence data points to more than USD 100 billion in hotel construction currently underway, with landmark properties including Aman Dubai, Janu Dubai, and Rosewood Dubai slated to open between 2027 and 2029, each allocating AED 50 to 200 million for interiors. Contract values at five-star properties exceed AED 17,000 per square metre, reflecting the premium fees that flow into the UAE interior design market.

The quality gap is what matters most for Western contractors considering entry. The volume of high-end luxury projects in Dubai demands a level of millwork engineering precision that relatively few local firms can deliver consistently at scale.

What Western contractors bring as standard, and what Dubai actively needs:

-

Millwork shop drawings built to North American or UK specification standards

-

SolidWorks 3D modelling and CNC-ready documentation

-

BIM-coordinated construction packages and Revit-level project documentation

-

Quality-assured estimating, procurement, and handover workflows

-

Compliance-ready technical packages aligned to Dubai Municipality 2026 approval processes

Dubai Municipality introduced more streamlined and digitally-driven fitout approval processes in 2026, focusing on compliance, safety, and sustainability. Firms that arrive with documentation workflows already aligned to these standards will carry a clear competitive edge. Read more about what this means practically in The Millwork Advantage section.

— Research and Markets, 2026

A Pause, Not a Retreat

The honest picture for Q1 2026 is a market that delivered extraordinary results in January and February, followed by a measured moderation in March. Sales in January reached AED 72.5 billion, up 62 percent year on year. February held positive at AED 61.4 billion, up 20 percent. March recorded AED 43 billion, a 6.4 percent dip compared to March 2025. That is a shift in pace, not a reversal in direction.

Harbor Real Estate’s Q1 2026 market report [5] frames this well: strong markets prove themselves in periods of uncertainty. The current rebalancing creates more attractive entry opportunities, particularly for buyers. It is a natural correction after a period of accelerated growth, not a structural break.

Dubai has a well-documented track record of absorbing external shocks and recovering with compound force. Following the 2008 global financial crisis, the emirate implemented regulatory reforms, diversified away from oil dependency, and delivered recovery cycles that rewarded those who stayed close to the market. Savills data shows the post-2020 pattern followed an almost identical script: a brief dip followed by one of the most expansive construction booms in the city’s history.

The macro framework underpinning Dubai’s growth remains fully intact. The Dubai Economic Agenda D33 targets making the city one of the world’s top three urban economies and doubling GDP by 2033. The IMF projects UAE GDP growth at 5.0 percent in 2026, the fastest in the GCC. Dubai’s population surpassed 4 million in 2025 and is expected to add up to 225,000 new residents in 2026 alone.

A View from the Ground

Earlier this year, I spoke with Sabby, a senior industry professional who recently finalised a joint venture with a well-regarded facade company to launch a fitout business in Dubai. The commercial logic was straightforward: facade work and interior fitout share supply chains, contractor relationships, and client trust. Moving from one into the other made natural sense.

What Sabby found was that even during this quieter phase, the volume of incoming leads and estimation requests was meaningful. The facade partner’s established reputation opened doors almost immediately. Many of those bids are currently in a holding pattern, with decision-makers who had an extended break through the March period only now returning to their desks and catching up on outstanding work.

That pattern is consistent with what we observe more broadly. The contractors positioning now, learning Dubai’s building codes, forming local relationships, and stress-testing their documentation workflows on Middle Eastern specifications, will be first in line when approval pace normalises. Sabby remains optimistic, and the data supports that view.

The Contrarian Case: Why This Phase Rewards Early Movers

Most contractors will wait for the recovery to be confirmed before they move. That is a reasonable instinct and also exactly why it tends to be the wrong one in markets like Dubai.

Here is what the current environment actually looks like for a well-prepared Western millwork contractor:

-

Entry and setup costs are more favourable than they were at 2024 peak pricing

-

Local partners are actively seeking credible international firms to strengthen their technical capability

-

The bid pipeline exists. Sabby’s experience confirms leads are flowing even in the quieter phase. The conversion timeline has lengthened, not the demand itself

-

Competitors who might have entered at peak pricing are reassessing. That creates breathing room for firms entering now to establish relationships and reputation before the volume returns

There is also a pricing discipline dimension that is easy to overlook. The current cost-sensitive environment is actually an advantage for firms that have tight estimation workflows and lean documentation operations. Clients who are budget-conscious right now are evaluating contractors more carefully on efficiency and technical capability, which is precisely where North American and UK millwork firms are strongest.

The bottom line: serious players do not wait for green lights. They use amber phases to build the foundations that generate returns when conditions improve.

Weighing the Decision: A Practical Overview

A phased or test-entry approach allows firms to evaluate the market while managing early-stage risk. The table below captures the key variables for USA, UK, and Canadian contractors currently thinking through their options.

| Why Evaluate Now | Points to Plan Around |

|---|---|

| Q1 2026 transactions up 31% year on year. Demand is structural, not speculative. | March 2026 saw a 6.4% monthly dip. Short-term pace moderation is worth monitoring. |

| USD 10B fit-out sector with a documented shortage of premium millwork capacity. | Over 1,500 registered fit-out companies create pricing competition at the mid-tier level. |

| January 2026 was the single highest real estate sales month in Dubai’s history. | Agile planning is needed as regional macro conditions continue to develop. |

| Dubai’s V-shaped recovery track record after 2008 and 2020 is well documented. | Cross-geography supply chain coordination requires early lead time planning. |

| Remote CAD and BIM support keeps overheads lean during a test-entry phase. | Dubai Municipality’s 2026 fitout approval updates require local regulatory familiarity. |

| IMF projects UAE GDP growth at 5.0% in 2026, the fastest rate in the GCC. | Some projects reflect near-term budget sensitivity as the market rebalances after rapid growth. |

Market entry assessment | UAE and Dubai | April 2026 | BluEnt analysis

Nobody times a market perfectly. What experienced contractors do is reduce exposure during uncertainty while increasing their positioning. Right now, Dubai offers both: a construction pipeline that has remained strong and a market where competition for premium millwork capacity has eased enough to allow careful, deliberate entry.

The Millwork Advantage: What Western Firms Bring

The technical depth that North American and UK millwork contractors bring to a project, precision shop drawings, SolidWorks 3D modelling, CNC-ready packages, BIM coordination, is not just a differentiator in Dubai. It is increasingly a requirement for the tier of projects that drive premium contract values.

The UAE interior fit-out market in 2026 is shaped by new sustainability requirements, smart building integration, and Dubai Municipality’s updated compliance framework. Western contractors who arrive with documentation standards already at this level, and who partner with technical support services that bridge the gap between North American and UK standards and UAE specifications, will be in the strongest possible position.

BluEnt has spent years providing millwork shop drawings, BIM coordination, SolidWorks modelling, and CAD support to contractors across North America and the UK. That same technical backbone translates directly into a competitive advantage in Dubai. To understand the market context that makes this relevant right now, revisit The Fitout Sector section or read about the contrarian entry case.

The Question Worth Sitting With

The firms that will lead the next phase of Dubai’s fitout and millwork market are already making moves. Some are running test bids. Some are forming joint ventures with local partners. Some are simply ensuring their CAD, BIM, and shop drawing workflows can handle Middle Eastern project specifications before the pace fully picks up. That groundwork takes time, and the contractors who do it now will have a real head start.

No one can predict the future with absolute certainty. Careful observation yields the best strategies. Dubai remains a market with structural demand, a proven recovery history, a government with every incentive to maintain and grow its global standing, and Q1 2026 data that continues to outperform most comparable global real estate markets.

As Dubai’s market evolves over the next 24 months, we are keen to build strong millwork partnerships. Connect with us to discover how our millwork services can add value to your projects.

Stay Tuned: We Are Watching This Closely

This remains an evolving situation. We are actively monitoring the Dubai fitout and millwork scenario and will continuously update this article as facts on the ground develop. The Q1 2026 data has been particularly encouraging and we will track Q2 closely as the full picture of this year’s market trajectory becomes clearer.

What are your thoughts on the UAE market? Are you holding off, or do you see this as a compelling entry window? Share your inputs and comments below. We would love to hear from you.

Authors:

Sources

-

Dubai Land Department: AED 761 Billion in Transactions in 2024

-

Dubai Land Department: Q1 2026 Real Estate Transactions, Dh252 Billion (April 2026)

-

Harbor Real Estate: Q1 2026 Dubai Market Report (Zawya, April 2026)

-

Edwards and Towers: Dubai Real Estate Market Q1 2026, Prices, Trends and Investment Insights

-

Cushman and Wakefield Core: Dubai Annual Market Update 2024 to 2025

-

Research and Markets: UAE Interior Fit-Out Forecast 2025 to 2030

-

Globe Newswire: UAE Interior Fit-Out USD 10B Opportunities 2026

-

Mordor Intelligence: UAE Interior Design Market 2025 to 2030

-

ECC Fit-Out: Top Interior Fit-Out Trends Shaping the UAE Market in 2026

-

Summertown Interiors: Commercial Fit-Out Contractors Guide 2026

-

Cavendish Maxwell: Dubai Residential Market Performance 2024

Millwork Drafting Trends You’re Going to See in 2026, According to Experts

Millwork Drafting Trends You’re Going to See in 2026, According to Experts  7 Stunning 3D Kitchen Design Ideas for a Perfect Remodel

7 Stunning 3D Kitchen Design Ideas for a Perfect Remodel  Outdoor Kitchen Designs and Cabinetry for Amenities Beyond Interiors

Outdoor Kitchen Designs and Cabinetry for Amenities Beyond Interiors  Kitchen Cabinet Trends Your Millwork Drafter Must Consider for Remodeling Projects

Kitchen Cabinet Trends Your Millwork Drafter Must Consider for Remodeling Projects